Technology Due Diligence is on the rise. Yet we are told that many investors struggle to understand the value of Tech DD.

Hence, this article provides the questions investors ask us as technology due diligence advisors.

I hope these questions are of value to you.

These questions will help you better understand the team, their plans and their ability to execute their vision.

Every investment is different, and your questions should be tailored to the company you’re examining. However, there are some key things you should always keep in mind during Technology Due Diligence.

Technology Due Diligence is more than a list of questions

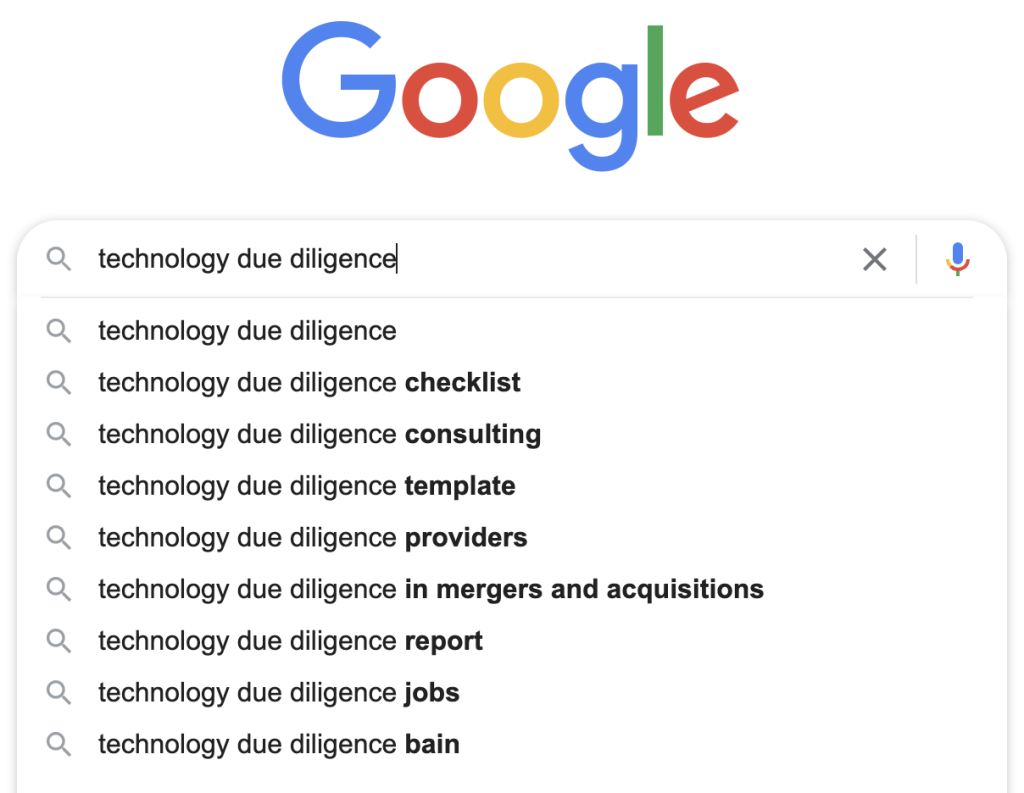

A quick check of Google to understand the searches made against “technology due diligence”. As per the image. the most popular searches are looking for checklists and templates:

But Technology Due Diligence is much more complicated than going through a pre-defined checklist. As establishing how technology provides value is a complex exercise.

We also believe that running these technology assessments cannot be sold by partners and then delegated to junior staff.

Instead, strong Technology Due Diligence assessors need to have C-Suite responsibility and sat on both sides of a PE deal. Ensuring they have the tech, people and commercial knowledge to make relevant observations and judgement.

A tailored diligence scope is essential for success

If technology due diligence is being considered, we typically assume the deal is someway progressed already. Because Tech DD is rarely bought into a deal early.

Instead of wading through hundreds of pre-defined questions, creating a high-level scope tailored to your deal is better. Typically this starts by understanding:

Your Investment Thesis

As we will work between you and the target, we need to understand both perspectives to be the most impactful.

We must determine how we can genuinely help you and not undertake an expensive ‘check box’ exercise. So we need to understand the rationale for the deal. Then check the assumptions you are making regarding the technology and the team.

The first discussion about the target business will outline the essential details. Such as the type of deal, e.g. Growth Cap, Buyout Secondary etc., the industry, the size etc. Followed by an initial discussion regarding the team and the underlying technology.

We need to know what value you believe the technology contributes to the business. And any growth assumptions technology fulfils now and in the future.

Typically, the tech provides value and operates as claimed by management. But scaling or cyber-security concerns today need addressing to meet the investor’s expectations.

Technology Due Diligence Scope

Once we understand your investment thesis and the target business, we can develop a detailed scope.

A good scope should ideally:

- Outline and detail all key themes for the engagement; we typically utilise seven themes

- Specify the timelines, key deadlines and initial meetings

- Who are the key stakeholders and those on the In The Know (ITK) List?

- Describe the 5-7 key questions specific to this target

- Take on board the investor’s preferences for the final report

- Agree how key observations will be presented

- Agree on the management briefing timings, whether in person or over Zoom/Teams etc.

- Remind the investor that the scope will probably change after the first two or three meetings

The typical questions we are asked by investors are stated below.

1. Is the technology ‘real’?

The technology may still be in its infancy with smaller or growth capital deals. So it’s fair to be considering this question.

In the early stages, there is often a misalignment between a founder’s pitch and what technology can do.

Plus, there are varying interpretations of what ‘artificial intelligence’ is and how it can create business value. Therefore, it makes perfect sense to de-risk this concern for future investors.

But contrary to belief, this question is valid, even with mature businesses in large deals.

For example, we have seen situations where the core IP critical to the deal was not created by the seller. This was due to employees moving on. The current staff did not understand the situation and technology fully.

Or, in the worst case, the tech simply was a few glossy screens with little technology built behind it.

2. Is the tech any good?

This is possibly a controversial and unfair question for the target as the answer will be subjective. But it is a common question that will undoubtedly be discussed with the investor.

As diligence providers, we are usually sat between two parties with different perspectives, yet both want the same outcome.

- Management tends to present a positive and cost-effective technology outcome. The ‘art of the possible’.

- In contrast, the investor prefers to see a more balanced view. Management needs to demonstrate risks have been considered adequately.

Hence the response to this ‘is it any good’ question is a subjective opinion. Based on a thorough, time-limited assessment of the entire technology department or function.

We respect that if a firm has PE attention, something ‘good’ is undoubtedly happening. But we also must keep an open mind that serious issues may be uncovered.

The response to this question is vital to both parties, so there’s much work behind the scenes to clarify.

3. How easy is it to replicate the technology?

Understandably, the ability of others to copy a technology solution/product is a critical concern for the investor.

So, we work on the basis of:

Anybody, with some money and skilled people, can copy anything.

This may sound a little defeatist. But this mindset forces us to uncover the periphery areas that secure the IP and business.

Often CTOs respond to this line of questioning by saying their systems are ‘big’ or complex. But that isn’t enough. As well-funded teams can address both.

So the key to defensibility is the human aspect. For example, partnerships with other firms and suppliers, especially if the relationships are exclusive. In one case, a firm had exclusive rights with BT that no one else can get. That type of agreement is gold dust.

The time, effort, and knowledge needed to create integrations with others are key from the technology perspective. Notably, the time it took to learn and perfect connections with others.

For example, in one Fintech, it took a couple of years to connect and perfect the messaging between partners. That situation was almost impossible to recreate as there was little appetite to spend more time on integration.

4. The CxO’s experience and ability to support intended growth

Investors want a professional opinion regarding the technology leader’s expertise, capability today and ability to support the future business plan.

This is an easier task if the CxO has previous experience in other PE-backed portfolio companies. Especially if we can find evidence of their contribution to growth in prior companies.

We need to assess their vision, leadership style and ability to drive the team. Interviewing the team can help bolster the observations, but this depends on who is on the ‘In the Know’ list.

Plus, there are many other factors to consider. Such as tenure, skin in the game, and whether the leader is more suited to startup or scale up.

HBR documents differences in their article How Your Leadership Has to Change as Your Startup Scales.

But we often observe people in transition. A technology leader who was excellent at startup and has managed to develop their skills to facilitate scaling the business.

But they are not ready for the next stage of growth. The increased pace, expectations and higher levels of governance that will activate as soon as the deal completes. Especially if there are new faces on the board.

In the past 18 months, we have interviewed and assessed many tech leaders who demonstrate high levels of humility. This is regardless of business size, industry and experience.

I believe humility is a key attribute necessary for a firm to succeed. As it leads to producing technology helps build a business attractive to Private Equity.

5. What is decision-making like, and how can it be improved?

Technology Strategy and the Product Roadmap are vital.

Yet, it’s not unusual for a target’s strategy to be weak, even in late-stage businesses with huge revenues. Sometimes non-existent.

Many firms work solely on trust and outline plans. Many do not have the rigour around decision making, spending and return on investment.

Often the tech leaders avoid planning. Some continue this post-investment and become targets for replacement.

We assess the plans, roadmaps and strategy to see how management made decisions in the past. Then extrapolate that to the forecast.

We also want to know how value attribution has been identified and tracked.

What is ‘value attribution?” Simply put, a clear understanding the benefit of technology effort and spending. Or ROI.

We also want to understand:

- Is the team identifying what to work on based on customer needs and ROI? Or on what they think should be developed?

- Has the team had any long-term projects that have failed? Or worse – tech projects that have succeeded technically but were rejected and not adopted by employees?

- The ratio of effort and spending just to keep the lights on.

6. What’s the maintenance ratio?

Here we assess how much of an investment will be used to keep the lights on versus innovation. There is no right number, and is related to your current business maturity and the growth plan.

Assessing the level of time, effort and spending spent on tech maintenance (versus net-new activity) is essential. Regardless of the size or maturity of the business.

Typically we find the ratio is typically out of kilter with the growth plan, which certainly needs to be understood.

What brings this to our attention is when the ratio is unusually low (10-20%) or high (>60%).

- If the ratio is ‘high’. We need to determine if the number is driven by the CFO (for, say, R&D and capitalisation purposes). Or maybe there are issues with the technology products.

- If the ratio is ‘low’. This could be due to product maturity or presenting the team as focused largely on innovation.

The IT Budget is integral to calculating this ratio. The IT Budget is always submitted late. So, we published this article on What goes in an IT budget for Tech DD?

7. Do you need a code review?

Many investors are keen for code to be scanned.

Code scanning tools can be expensive and depend on the investor’s risk appetite. We find a spot-check of the repository by an experienced developer is usually enough.

Performing a high-level code assessment by checking the repositories is undoubtedly helpful. It enables us to understand the team’s history and cadence, and we can comment on quality.

But of course, you need ‘hands-on’ assessors if you are to rely on a consultant’s opinions.

8. How will it scale?

Sure, the pitch deck or information memorandum will show a growth story. But it is primarily a pitch document from management.

So we need to take a cynical view. We must understand how tech supports the growth journey and what is needed to achieve projections.

The cloud provides instant and global scaling of tech products. But the tech needs to be designed correctly and use the correct components. Otherwise, it can cost you a fortune in the long run.

It’s also common for teams to be aware of cost optimisation opportunities. But they are too focused on creating new features for customers. So these optimisations are not enabled.

Enabling the optimisation could be complex. But, often the teams are unaware of the costs of achieving this.

Scaling the tech and operations team when wage inflation and staff attrition are high. Hence, it is essential to understand those plans and note if they are appropriate to the firm’s culture and industry.

For instance, it’s not worth applying a Fintech hiring strategy to a manufacturing tech solution. As wages, perception and culture will be different and attract another type of staff.

But the most common scaling concern is people. If either professional services or operations teams need to grow as the revenues grow, this could be a red flag.

And the added burden of increased management and retention needs to be considered.

Other questions to consider during Technology Due Diligence

The great thing about this job is the vast areas that must be considered as a technology due diligence assessment.

It’s fascinating and an honour to be able to access, review and advise on how a technology team operates. How they provide value today and what the future looks like.

We have hundreds of questions we can ask a target; but here are some high-level themes below:

- What is the size and complexity of the IT estate? – You need to understand what you’re dealing with regarding technical debt, supportability and future commercial risks.

- Who are the critical suppliers, and what is the commercial relationship? You need to understand if there are any contractual risks and how easy it would be to switch.

- How is IT funded, and what’s been done with that money? You need to match technology spending with the historical performance & forecast.

- What is the team culture like, and how does it impact delivery? You need to know if the team are working towards the same goal and that they have the right skills to achieve it.

- How mature are their processes, and what does this mean for you? – You need to understand how well the team works together and what kind of processes drive the team’s output.

- What are the risks, and how are they being managed? – You need to identify potential risks that could impact the project’s success and understand how they are managed.

- What is their governance model? – You need to know who makes decisions about the project and how those decisions are made. Knowing this will help you understand the team’s decision-making.

- Cyber is, of course, a vast topic. So how are they managing it? You need to understand how the team manages cyber security risks with all the news about data breaches.

Technology Due Diligence is an art.

You need a clear management report that articulates the risks and highlights potential opportunities. Yet Technology Due Diligence is a growing field but one that is not without its challenges.

Collecting the correct information and facts and providing a professional, balanced and insightful opinion across a business is essential.

The ‘art’ here is asking the right questions that are pertinent to the situation and of value to the investor.

If you’re interested in learning about technology due diligence, read our whitepaper “Five questions EVERY investor should ask about technology“.

This paper provides the standard questions we typically see investors asking and five questions that may be insightful during a deal’s early processes.

For information written for Tech Leaders within the target business, please refer to this guide to Tech DD for Tech Leaders.